CTC vs In-Hand Salary: Complete Breakdown for Indian Employees 2026

MoneyUtility Team

Compensation Specialist

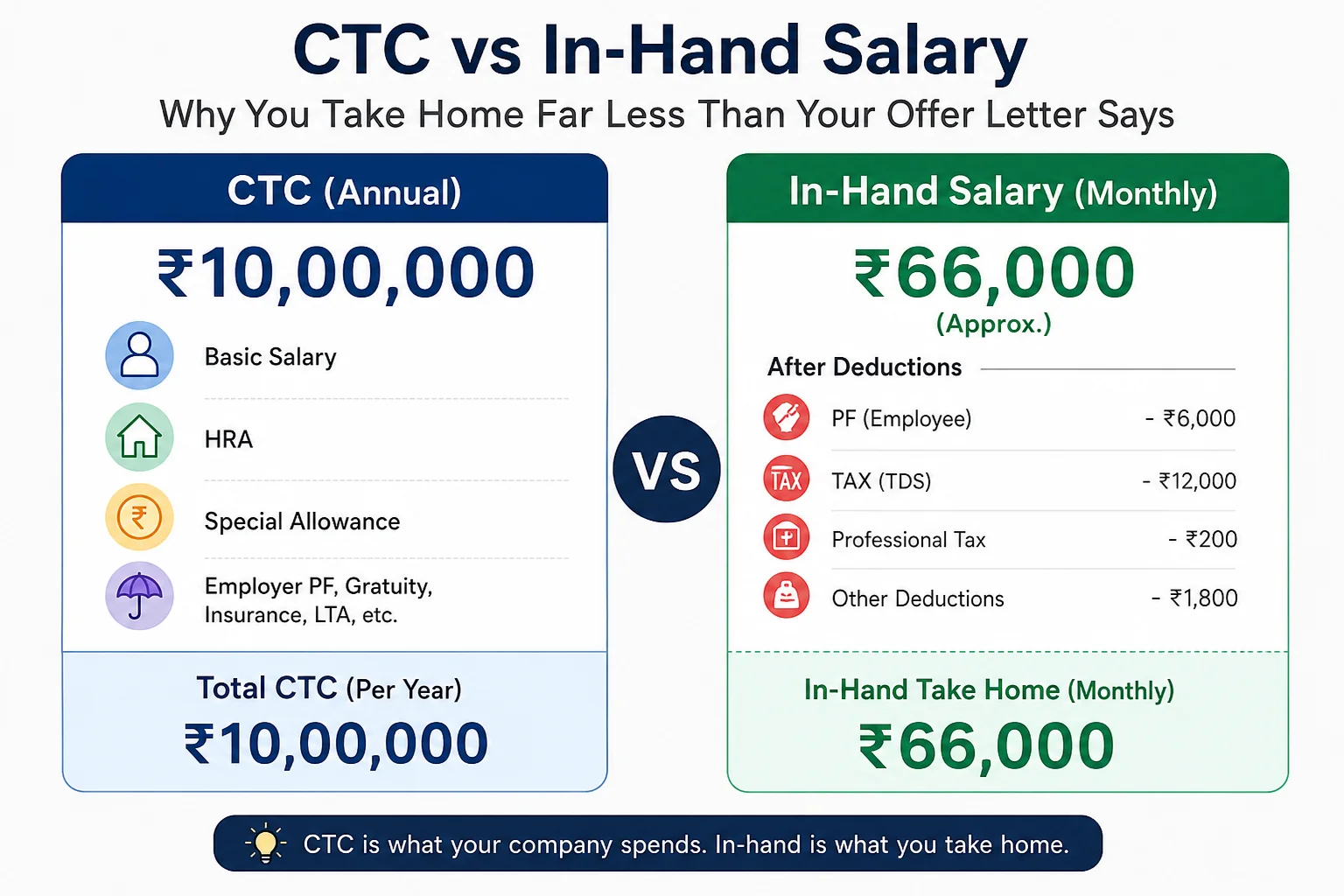

1. That ₹10 Lakh Offer Letter vs Your First Salary Slip

Landing your first job or receiving a fresh appraisal letter is always an exciting milestone. When you see a handsome Cost to Company (CTC) figure like ₹10,00,000 per annum, your immediate reaction might be to divide it by 12 and expect around ₹83,333 to hit your bank account each month. However, the reality of a paycheck is often a cold shower for freshers. The huge difference between your CTC vs in-hand salary India calculations can leave you shocked when your first salary slip shows only ₹66,000 or ₹69,533.

Where does that difference go? Why does a ₹10 LPA offer translate to a monthly take-home salary that is nearly ₹14,000 less than expected? The answer lies in how compensation packages are structured in India. Your offer letter contains multiple components that are not direct cash, plus statutory deductions that occur before the money reaches your pocket. In this guide, we will break down every rupee that goes missing, so you can evaluate job offers with clarity and avoid bad surprises on pay day.

Table of Contents

2. What Exactly is CTC?

Cost to Company (CTC) is a term that refers to the absolute cumulative expenditure an employer incurs on employing an individual. When an HR representative shares your CTC, they are telling you how much your employment will cost the business financially over a year.

It is critical to understand that CTC is NOT the salary you receive. Instead, it is a bundle of multiple direct, indirect, and future retiral benefits. These components are grouped into the CTC to present an attractive overall figure, even though many of them will never reach your bank account as monthly cash. Common non-cash components included in your CTC are:

- Employer Provident Fund (EPF) Contribution: The 12% contribution that your employer makes towards your EPF account is added directly to your CTC.

- Gratuity Provision: A statutory retirement benefit that the company sets aside annually on your behalf, usually valued at 4.81% of your Basic Salary.

- Group Medical Insurance Premium: The insurance premium paid by the company to cover you and your dependents.

- Meal Coupons / Food Coupons: The face value of meal cards (like Sodexo) that are offered as tax-free options but reduce your net cash payout.

- Employer NPS Contribution: Any voluntary pension savings made by the employer under Section 80CCD(2).

3. What is In-Hand (Take-Home) Salary?

Your In-Hand (Take-Home) Salary is the net cash amount that is deposited into your bank account on pay day. This represents your actual spending power each month. To arrive at this number, we must start with your Gross Salary (which is CTC minus the employer-side benefits like employer PF and gratuity) and subtract all employee-side deductions.

The mathematical formula to define your take-home pay is:

Let us define each of these deductions briefly:

- Gross Salary: The total amount of direct pay consisting of Basic Salary, House Rent Allowance (HRA), Special Allowance, and other flexi components.

- Employee PF: The mandatory contribution of 12% of your Basic Salary that is deducted from your gross pay and deposited into your EPFO account.

- Professional Tax (PT): A state-government tax levied on salaried professions, capped at a maximum of ₹2,500 per year (usually deducted as ₹200 per month).

- TDS (Tax Deducted at Source): The monthly income tax deducted by your employer based on your projected annual income tax liability.

- ESI (Employee State Insurance): A mandatory health scheme contribution of 0.75% of gross salary, applicable only to employees whose gross salary is up to ₹21,000 per month.

4. Complete CTC to In-Hand Calculation — ₹10 Lakh CTC Example

If you want to know how to calculate in-hand salary from CTC, the process starts by identifying how your company constructs your payroll components. Let's look at a detailed example of an employee working in a metro city (Mumbai or Delhi) earning a gross CTC of ₹10,00,000 per annum. We assume they are evaluated under the default New Tax Regime for FY 2025–26 (and 2026), have standard deductions, and are not subject to ESI.

Section A — CTC Breakup (Annual and Monthly)

| Component | Monthly (₹) | Annual (₹) | Part of CTC? |

|---|---|---|---|

| Basic Salary (40% of CTC) | ₹33,333 | ₹4,00,000 | Yes |

| House Rent Allowance (HRA - 50% of Basic) | ₹16,667 | ₹2,00,000 | Yes |

| Special Allowance | ₹22,530 | ₹2,70,360 | Yes |

| Leave Travel Allowance (LTA) | ₹2,000 | ₹24,000 | Yes |

| Food Coupons (Flexi benefit) | ₹2,200 | ₹26,400 | Yes |

| Employer PF (12% of Basic) | ₹4,000 | ₹48,000 | Yes |

| Employer NPS Contribution | ₹0 | ₹0 | Yes |

| Gratuity Provision (4.81% of Basic) | ₹1,603 | ₹19,240 | Yes |

| Group Medical Insurance Premium | ₹1,000 | ₹12,000 | Yes |

| Total CTC: | ₹83,333 | ₹10,00,000 | Total Cost |

To calculate the actual Gross Salary, we subtract non-cash components that go directly to insurance providers, retirement bodies, or future accruals. Therefore, Gross Annual Salary = ₹10,00,000 (CTC) − ₹48,000 (Employer PF) − ₹19,240 (Gratuity) − ₹12,000 (Insurance) = ₹9,20,760. This works out to a Gross Monthly Salary of ₹76,730.

Section B — Deductions from Gross Salary

| Deduction Component | Monthly Amount (₹) | Annual Amount (₹) |

|---|---|---|

| Employee PF Contribution (12% of Basic) | ₹4,000 | ₹48,000 |

| Professional Tax (State-specific) | ₹200 | ₹2,400 |

| Income Tax / TDS (under New Regime slabs) | ₹2,997 | ₹35,959 |

| Total Deductions: | ₹7,197 | ₹86,359 |

Now we calculate the final take-home: In-Hand Monthly = Gross Monthly (₹76,730) − Total Monthly Deductions (₹7,197) = ₹69,533.Thus, for a ₹10 Lakh offer, your actual in-hand pay is exactly ₹69,533 per month, while the remaining ₹13,800 per month is diverted to taxes, professional fees, and your retirement portfolio.

5. The 5 Biggest Deductions That Shrink Your Take-Home

Understanding where your hard-earned cash is routed is the first step to financial planning. Navigating the maze of salary deductions India 2026 guidelines is key. Let us look at the five primary factors that shrink your net paycheck:

Employee Provident Fund (EPF)

The EPF deduction salary component goes directly into your retirement fund. By law, both you and your employer must contribute 12% of your Basic Salary + Dearness Allowance (DA) to your EPF account. While this deduction reduces your immediate take-home pay, it is a risk-free investment that earns a compounding interest rate backed by the government. If your Basic Salary is up to ₹15,000 per month, this deduction is statutory and mandatory.

Income Tax (TDS)

Tax Deducted at Source (TDS) is your monthly installment of income tax. Employers are legally obligated to deduct this tax before depositing your salary. The exact TDS amount is determined by your total annual taxable income and whether you select the old or new tax regime. You can model different configurations and tax outgos using our free Income Tax Calculator.

Professional Tax

Professional Tax is a state-level levy on professionals, merchants, and salaried employees. Not all states charge professional tax. In states that do (such as Maharashtra, Karnataka, Tamil Nadu, and West Bengal), the maximum amount is capped by the Constitution of India at ₹2,500 per year, usually deducted as ₹200 per month (and ₹300 in the final month).

ESI (Employee State Insurance)

Employee State Insurance is a statutory social security and health insurance scheme in India. It is mandatory for employees whose gross monthly salary is up to ₹21,000. The employee contributes 0.75% of their gross salary, and the employer contributes 3.25% of the gross salary. Employees earning higher salaries are exempt from ESI deductions.

Gratuity Provision

A gratuity provision is a statutory benefit paid by employers under the Payment of Gratuity Act, 1972. It is a provision set aside at 4.81% of your Basic Salary. Even though companies add it to your annual CTC, you only receive it in cash when you leave the company after completing at least 5 continuous years of service. If you resign earlier, you forfeit this entire amount.

6. CTC vs In-Hand Salary India Across Salary Levels

To show how deductions scale as income increases, let us look at a comprehensive comparison. Using a free take home salary calculator India employees can model how different offer levels convert to real cash in hand.

Below is a comparison table across four common annual CTC levels under the New Tax Regime (assuming standard structure of Basic at 40% of CTC, no other flexible benefits, and standard deductions):

| CTC (₹/year) | Approx Gross Monthly (₹) | Est. Deductions (₹/month) | Est. In-Hand Monthly (₹) | In-Hand as % of CTC |

|---|---|---|---|---|

| ₹5,00,000 | ₹38,365 | ₹2,200 | ₹36,165 | 86.8% |

| ₹8,00,000 | ₹61,351 | ₹3,400 | ₹57,951 | 86.9% |

| ₹12,00,000 | ₹92,276 | ₹9,753 | ₹82,523 | 82.5% |

| ₹20,00,000 | ₹1,54,210 | ₹27,497 | ₹1,26,713 | 76.0% |

💡 Tip: Note that these figures are indicative. The actual deductions will vary depending on your city category, choice of tax regime, and voluntary savings. You can use our interactive Salary Calculator to check your precise numbers.

7. Components in CTC That You Never Actually "Receive"

When reviewing your package, watch out for the components that are added to inflate the CTC number but do not represent actual disposable cash.

- Employer PF: This component is added to your CTC as a benefit. However, the money is transferred directly to the Employees' Provident Fund Organisation (EPFO). You can only access this amount upon retirement, during home purchases, or when you are unemployed for over 2 months.

- Group Health Insurance: Companies include the medical premium paid to group insurance brokers as part of your compensation package. This is a non-cash benefit that covers your medical treatments but cannot be spent on monthly bills.

- Gratuity Accrual: Calculated at 15/26 of your basic salary for every year of service. Companies add this to your annual CTC, but the payout is legally locked.

⚠️ Note: Gratuity provision is a non-cash accrual that only gets paid if you complete 5 continuous years of service at the company. Many freshers assume it's part of their monthly paycheck, but it is actually a retiral benefit you cannot access earlier.

8. How to Read Your Salary Slip Correctly

Understanding the difference between gross vs net salary India is essential for managing your money. A standard salary slip in India is divided into two primary columns: the **Earnings** side and the **Deductions** side.

- Earnings Side: Contains cash components paid directly to you. This includes:

- Basic Salary: The core taxable base of your compensation.

- HRA: Allocated for housing rental expenses.

- Special Allowance: A fully taxable balancing allowance.

- Conveyance & Other Allowances: Fixed allowances for travel or operational costs.

- Deductions Side: Contains statutory and non-statutory cuts. This includes:

- EPF Contribution: Employee contribution (usually matching employer's 12% of basic).

- Professional Tax: State-level service tax of ₹200.

- TDS: Tax Deducted at Source for federal income taxes.

- ESI: Deducted only if your gross salary is under the statutory limit.

To calculate your net take-home pay, simply subtract the sum of the deductions from the sum of the earnings: Net Pay = Total Earnings − Total Deductions.

💡 Tip: Keep your monthly salary slips saved securely. They are critical documents when applying for home loans, personal loans, credit cards, or when filing your annual Income Tax Return (ITR).

9. Tips to Maximise Your In-Hand from the Same CTC

If your current in-hand salary is low, you do not always need a salary hike to take home more cash. You can legally restructure your existing package to reduce taxes and maximize your pay. Read our complete salary structure optimization guide for detailed advice, or review these five simple tips:

- Optimize Your Basic Salary: Keep your Basic Salary at exactly 40% of your total CTC. This reduces your mandatory PF deductions (which are calculated as 12% of basic), thereby increasing your monthly cash in hand, while still keeping a healthy base for HRA and gratuity.

- Maximize HRA Claims: Renting a house? Align your HRA component to match your actual rent. You can calculate your tax exemptions using our free HRA Calculator to legally save tax and boost take-home pay.

- Opt for Food Coupons: Opt for tax-free meal vouchers (like Sodexo) worth up to ₹2,200 per month (₹50 per meal, 2 meals a day for 22 working days). This entire amount is excluded from your taxable income.

- Claim Phone and Internet Reimbursements: Request telephone and broadband internet bills to be reimbursed directly instead of being paid as a fully taxable allowance. This converts up to ₹24,000 per year of taxable income into a tax-free benefit.

- Leverage Employer NPS Contributions: Ask your employer to contribute up to 10% of your Basic Salary to the National Pension System (NPS) under Section 80CCD(2). This contribution is completely tax-free and helps you save for retirement while lowering your TDS liability.

10. Frequently Asked Questions About CTC vs In-Hand

How much in-hand salary will I get from ₹10 LPA CTC?

On a CTC of ₹10,00,000 per annum, your actual net monthly take-home salary will typically range between ₹63,000 and ₹70,000. The exact amount depends on your company's flexible benefit options, city category (metro vs non-metro), and whether you file taxes under the old or new tax regime.

Is CTC the same as gross salary?

No, CTC (Cost to Company) and Gross Salary are different. CTC includes all costs incurred by the employer, including employer contributions to PF, gratuity provisions, and group medical insurance. Gross Salary is the amount you see before employee-side deductions (like PF and tax) but after removing employer-side contributions.

Can I negotiate CTC structure at the time of offer?

Yes, most companies allow you to negotiate your CTC structure when they make a job offer. You can request HR to increase your HRA percentage, opt for a Flexible Benefit Plan (FBP) including food coupons, or include telephone and LTA reimbursements to minimize taxes and maximize your monthly take-home pay.

Does PF deduction reduce my in-hand salary?

Yes, both employer and employee PF contributions reduce your immediate monthly take-home pay. The employee contribution of 12% is deducted directly from your gross salary. However, this is not a lost expense; the money is transferred to your EPFO account and continues to build a high-yield retirement corpus.

What is professional tax and who pays it?

Professional Tax is a state-level tax levied on salaried employees and professionals. It is deducted by your employer from your gross salary and paid to the state government. The maximum amount is capped at ₹2,500 per year, and it is a deductible expense under Section 16(iii) of the Income Tax Act.

11. Conclusion

In conclusion, understanding the core dynamics of your CTC vs in-hand salary India calculations is essential for every salaried employee. By recognizing how non-cash components and statutory deductions reduce your offer letter figures, you can negotiate better and plan your savings effectively. To model your own salary components and identify tax-saving opportunities, calculate your take-home pay today.