Flat vs Reducing Interest Rate: Which Loan Costs More in India 2026?

MoneyUtility Team

Senior Personal Finance Writer

If you are planning to take a loan in India, understanding the choice between a flat vs reducing interest rate India is the most crucial decision you will make. At first glance, a 10% interest rate seems identical regardless of how it is calculated, but this small detail can cost you over ₹50,000 or even ₹1,00,000 in excess interest payments. Imagine you are presented with two loan offers. Lender A offers a ₹5,00,000 personal loan at 10% flat interest rate for 5 years. Lender B offers the exact same ₹5,00,000 personal loan at 10% reducing balance interest rate for 5 years. To the untrained eye, both loans look identical because they share the same interest rate and tenure. However, the resulting monthly EMI and the total interest outgo are dramatically different, exposing a hidden loan trap that catches millions of Indian borrowers off guard every year.

Table of Contents

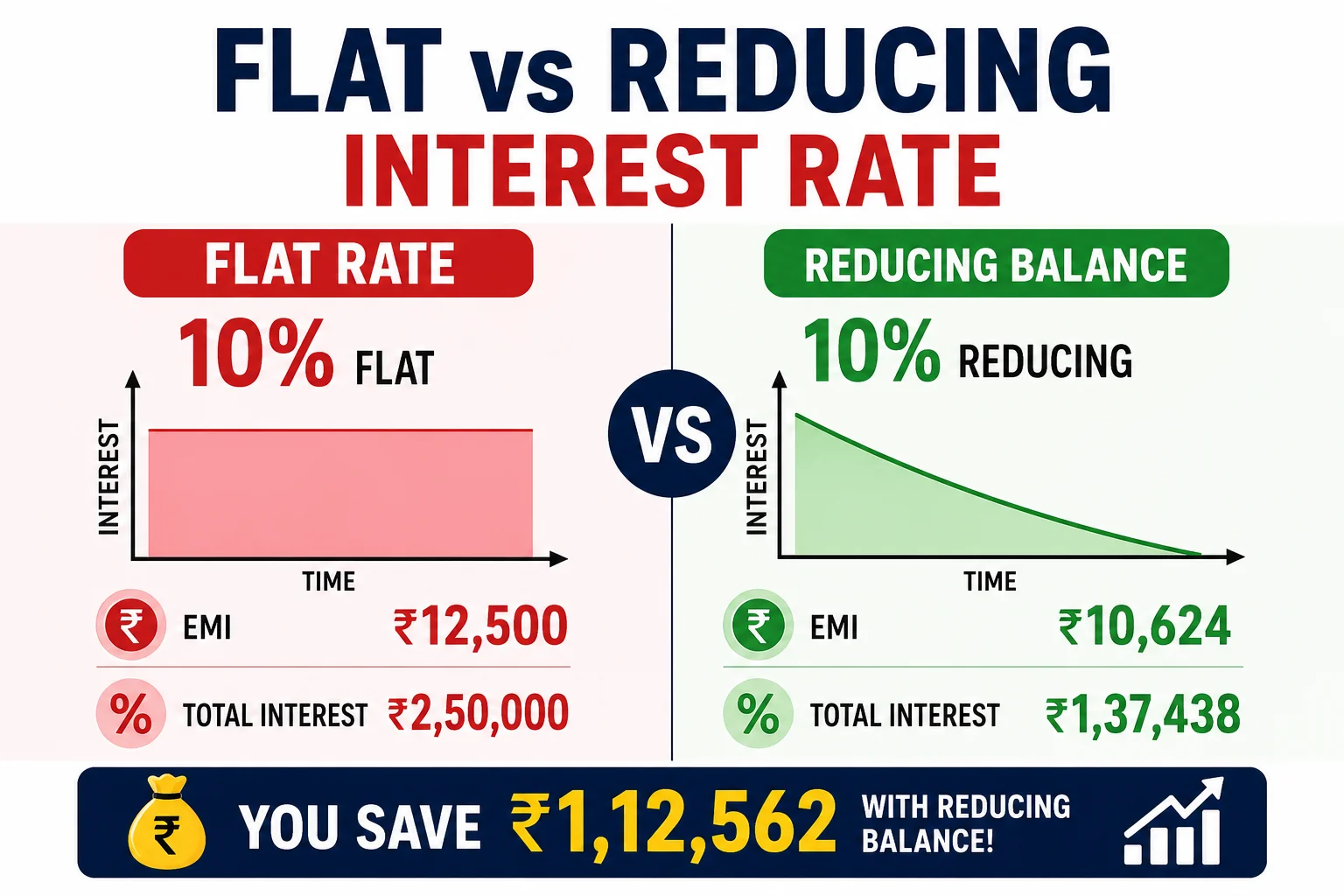

1. The Lender Said 10%. But Which 10%? This Distinction Could Cost You ₹50,000

When borrowing money, we are trained to scan the terms for the lowest interest rate percentage. However, the percentage itself is only half of the story. The method used to calculate that interest determines how much hard-earned cash you will actually pay over the life of the loan. In our initial example, Lender A's flat rate of 10% forces you to pay ₹12,500 every month, yielding a total interest outgo of ₹2,50,000. On the other hand, Lender B's reducing rate of 10% yields a monthly payment of ₹10,624, and a total interest outgo of ₹1,37,411.

Choosing Lender A means you are throwing away an extra ₹1,12,589 in interest payments alone! This distinction does not just cost you ₹50,000; on a typical 5-year personal loan of ₹5,00,000, it costs you more than double that amount. To understand why this happens, we must dissect the mathematical models behind both methodologies.

2. What Is a Flat Interest Rate?

Under a flat interest rate regime, the interest is calculated on the original principal amount for the entire duration of the loan tenure. The critical detail to understand is that the interest amount remains exactly the same every month, regardless of how much of the loan principal you have already repaid.

The mathematical formula to calculate the monthly interest under this method is:

Where:

- P = Original Principal Loan Amount

- R = Flat Annual Interest Rate (in percentage)

- T = Loan Tenure in Years

Worked Example: ₹5,00,000 Loan at 10% Flat Rate for 5 Years

Let's calculate the real numbers for a flat rate loan:

- Calculate Total Interest:

Total Interest = ₹5,00,000 × 10% × 5 = ₹2,50,000 - Calculate Total Repayment Amount:

Total Amount = Principal + Interest = ₹5,00,000 + ₹2,50,000 = ₹7,50,000 - Calculate Monthly EMI:

EMI = Total Amount ÷ 60 Months = ₹7,50,000 ÷ 60 = ₹12,500/month

Flat rates are commonly used for gold loans, personal loans from certain Non-Banking Financial Companies (NBFCs), vehicle financing, and informal microfinance lenders.

3. What Is a Reducing Balance Interest Rate?

With a reducing balance interest rate, the interest is calculated only on the outstanding principal balance of the loan, which decreases every time you make an EMI payment. As you repay the principal, the outstanding amount shrinks, and consequently, the monthly interest portion decreases. This is the industry standard for home loans, car loans from retail banks, and personal loans from tier-1 commercial banks.

The reducing balance monthly EMI is calculated using the following standard amortization formula:

Where:

- P = Principal Loan Amount (₹5,00,000)

- r= Monthly Interest Rate. Calculated as: Annual Rate ÷ 12 ÷ 100 (For 10%, r = 10 ÷ 12 ÷ 100 = 0.00833)

- n = Loan Tenure in Months (For 5 years, n = 60 months)

Worked Example: ₹5,00,000 Loan at 10% Reducing Rate for 5 Years

Let's calculate the exact figures under the reducing balance method:

- Calculate Monthly Interest Rate (r):

r = 0.00833333 - Apply the Formula for EMI:

EMI = [₹5,00,000 × 0.00833333 × (1.00833333)^60] ÷ [(1.00833333)^60 − 1]

EMI = ₹10,624 (specifically ₹10,623.52) - Calculate Total Repayment Amount:

Total Amount Paid = ₹10,623.52 × 60 Months = ₹6,37,411 - Calculate Total Interest Paid:

Total Interest Paid = ₹6,37,411 − ₹5,00,000 = ₹1,37,411

Comparing this directly to the flat rate loan, the flat rate charges ₹2,50,000 in interest while the reducing balance method charges only ₹1,37,411. This means you save a massive ₹1,12,589 in interest payments by choosing a reducing balance loan.

4. The Shocking Side-by-Side Comparison

To truly understand how deep this calculation gap is, we must look at a direct flat rate vs reducing balance rate comparison. Let's compare a ₹5,00,000 loan over a 5-year tenure at a quoted rate of 10%.

| Feature | Flat Rate (10%) | Reducing Balance (10%) |

|---|---|---|

| Monthly EMI | ₹12,500 | ₹10,624 |

| Total Interest Paid | ₹2,50,000 | ₹1,37,411 |

| Total Amount Repaid | ₹7,50,000 | ₹6,37,411 |

| Effective Annual Cost (APR) | 17.27% | 10.00% |

| Interest Saving | N/A | ₹1,12,589 |

This comparison highlights the core of the problem: a flat interest rate makes the loan look nearly half as expensive as it actually is. The borrower feels they are getting a great deal at 10%, but in reality, they are paying an interest burden equivalent to a 17.27% reducing balance interest rate.

5. The Conversion Formula: Flat Rate to Reducing Rate

When you are shopping around for personal loans, vehicle financing, or gold loans in India, lenders will quote different rate types. To make an apples-to-apples comparison, you must learn how to convert flat rate to reducing rate.

A quick, highly effective conversion rule of thumb for a 5-year loan is:

This multiplier varies depending on the loan tenure. For a 1-year loan, the multiplier is roughly 1.8, whereas for a 7-year loan, it rises to around 1.9.

For a highly accurate conversion, financial analysts use the Internal Rate of Return (IRR) method. The IRR is a method of calculating the exact rate of interest that makes the net present value of all cash outgoes (monthly EMIs) equal to the loan principal received. Under a flat rate loan, because you pay the same interest portion even as the principal is returned, you are deprived of the use of that capital, which drastically increases the IRR.

| Flat Rate (%) | Approximate Equivalent Reducing Rate (%) | Tenure Assumed |

|---|---|---|

| 8% flat | ~15% reducing | 5 Years |

| 10% flat | ~18% reducing | 5 Years |

| 12% flat | ~21% reducing | 5 Years |

| 14% flat | ~25% reducing | 5 Years |

| 15% flat | ~27% reducing | 5 Years |

6. Month-by-Month Interest Breakdown: Flat vs Reducing

To visually demonstrate how the flat rate disadvantages you, let's trace the first 6 months of a ₹5,00,000 loan at a quoted interest rate of 10% over a 5-year tenure. The flat rate borrower pays ₹12,500 per month, with interest fixed at ₹4,167. The reducing rate borrower pays ₹10,624, and interest changes dynamically.

| Month | Opening Balance (₹) | Flat Rate Interest (₹) | Reducing Balance Interest (₹) | Difference (₹) |

|---|---|---|---|---|

| 1 | ₹5,00,000 | ₹4,167 | ₹4,167 | ₹0 |

| 2 | ₹4,93,543 | ₹4,167 | ₹4,113 | ₹54 |

| 3 | ₹4,87,032 | ₹4,167 | ₹4,059 | ₹108 |

| 4 | ₹4,80,468 | ₹4,167 | ₹4,004 | ₹163 |

| 5 | ₹4,73,848 | ₹4,167 | ₹3,949 | ₹218 |

| 6 | ₹4,67,173 | ₹4,167 | ₹3,893 | ₹274 |

In Month 1, both lenders charge ₹4,167 interest. However, by Month 6, the reducing balance interest drops to ₹3,893, creating a difference of ₹274 in that month alone. The difference continues to grow month after month. Fast forward to Month 60 (the final month of the loan): the flat rate borrower is still charged the exact same interest of ₹4,167, even though the outstanding balance is almost zero (around ₹12,500). Meanwhile, the reducing rate borrower pays a tiny interest portion of only ₹88 in the final month.

This stark contrast is why flat rate loans cost so much more: you are forced to pay maximum interest on capital you have already returned to the lender months or years prior.

7. Where You'll Encounter Each Rate Type in India

To successfully navigate the credit market, you need to know where lenders employ these calculation methods. Lenders compete heavily, and some exploit flat interest rates to attract borrowers with deceptively low numbers. Here is a personal loan interest rate comparison India 2026 analysis by loan product:

| Loan Type | Common Rate Method | Why |

|---|---|---|

| Home Loans (Banks) | Reducing Balance | Mandated by the RBI for retail lending; long tenures make flat rates math-prohibitive. |

| Car Loans (Banks) | Reducing Balance | Regulated banks use standard reducing balance interest rates. |

| Personal Loans (Major Banks) | Reducing Balance | HDFC, ICICI, SBI, and Axis use reducing rates for personal credit. |

| Gold Loans | Flat (Often) | Usually short-term, quick processing. NBFCs leverage flat rates. |

| Vehicle Loans (NBFCs) | Often Flat — Verify | NBFCs financing commercial vehicles or used cars frequently quote flat. |

| Two-Wheeler Loans | Often Flat | Small ticket sizes. Dealership partnerships usually feature flat structures. |

| Microfinance Loans | Flat | Common in rural lending; simple flat calculations are easy to market. |

| Credit Card EMI Conversion | Reducing (but high rate) | Structured as reducing balance, but the rates are high (13-18%). |

8. How to Compare Two Loan Offers with Different Rate Types

Lenders will often try to confuse you by mixing terminologies. However, as an analytical borrower, you can cut through the noise by focusing strictly on the actual rupee outgo. Here is a step-by-step guide to comparing any two loan offers:

- Step 1: Ask each lender: "Is this flat or reducing balance rate?"

- Step 2: Get the monthly EMI in writing: Never rely on estimates; obtain the final, binding EMI figure quoted for your principal and tenure.

- Step 3: Calculate the total amount paid: Multiply the monthly EMI by the total number of months in the loan tenure:

Total Repayment = Monthly EMI × Tenure (in months) - Step 4: Calculate the total interest cost: Subtract the principal loan amount from the total repayment amount:

Total Interest Cost = Total Repayment − Principal Amount - Step 5: The lower total interest option wins: The loan option that charges you the lowest total interest amount is the cheaper offer, regardless of what rate percentage the lenders quote.

To verify these figures, you can use our free online tools. Our EMI Calculator is designed to help you verify reducing balance interest schedules, and our home loan calculator can assist with long-term home credit calculations.

9. Practical Tips to Avoid the Flat Rate Trap

Protecting yourself from the marketing tricks of aggressive lenders requires discipline. Use these six actionable tips to ensure you never overpay for your loan:

- Always ask explicitly: "Is this flat or reducing balance rate?" Push for a written response from your relationship manager.

- Calculate the total interest cost: Multiply the quoted EMI by the tenure months and subtract the principal. Do not let the quoted rate percent distract you.

- Request the amortization schedule: Ask for a copy of the month-by-month repayment table before signing the agreement. A reducing rate amortization schedule will show the interest component dropping every month.

- Be extra cautious with NBFCs and dealers: Gold loan companies, local vehicle finance dealers, and non-bank lenders frequently advertise flat rates to sound competitive with public bank rates.

- Check the APR: Regulated lenders must disclose the APR in their loan documents. The APR represents the true reducing rate cost plus additional fees.

- Use the EMI Calculator: Always verify the lender's quoted monthly EMI against a standard online reducing balance formula. If you need help calculating the monthly figures manually, refer to our detailed EMI calculation guide.

Additionally, remember that loan duration has a major impact on total interest outgo. Check our loan tenure impact guide to see how choosing the right timeline can save you lakhs. Finally, before applying, make sure your credit score is in order by reading our credit score guide.

10. Frequently Asked Questions: Flat vs Reducing Interest Rate

What is the difference between flat rate and reducing balance rate?

A flat interest rate calculates interest on the original loan amount for the entire tenure, meaning interest charges remain constant. A reducing balance rate calculates interest only on the outstanding principal balance, which decreases with every monthly repayment, resulting in a much lower overall cost.

Which is better, flat or reducing interest rate?

A reducing interest rate is always better and cheaper for the borrower. Even if both rates are quoted at the same percentage (e.g., 10%), a reducing balance loan will cost significantly less in total interest compared to a flat rate loan because you only pay interest on the money you still owe, rather than the initial amount.

How do I convert flat interest rate to reducing interest rate?

You can convert a flat rate to an approximate reducing rate using the multiplier method. For a standard 5-year loan, the equivalent reducing rate is approximately Flat Rate multiplied by 1.85. For instance, a 10% flat rate is equivalent to a reducing rate of approximately 18% (specifically 17.27%). More precise conversions require the Internal Rate of Return (IRR) method.

Do banks in India charge flat or reducing interest rates?

Most regulated commercial banks in India (such as SBI, HDFC, and ICICI Bank) charge reducing balance interest rates for major retail loan products, including home, car, and personal loans. However, some Non-Banking Financial Companies (NBFCs), vehicle dealerships, and microfinance institutions may still quote flat rates to make their interest rates appear artificially low.

Is gold loan interest flat or reducing?

Gold loan interest structures vary by lender and scheme in India. Many local gold loan providers and NBFCs charge flat rates, where the interest is calculated on the initial loan amount. However, major banks offering gold loans often use the reducing balance method or a bullet repayment scheme where interest is compounded monthly on the outstanding balance.

11. Conclusion

When navigating the Indian credit market, understanding the difference between a flat vs reducing interest rate India can save you tens of thousands of rupees. A flat rate interest structure remains one of the oldest marketing tricks used to make high-cost loans look incredibly affordable. By focusing on the total interest paid and utilizing the equivalent reducing rate conversion, you can easily protect yourself from these financial pitfalls. Never sign a loan agreement without verifying the calculations yourself using our online tools.